In today’s financial world, various banks and financial institutions are waiting for potential customers to sell their credit card or give loans. The offers seem so alluring at first, but they might have certain hidden agendas that can prove harmful to you in the long run. So, it is better to take precaution, rather than being sorry later on. We, at Credit Bazaar, have illustrated a list of common crediting traps that are widespread today, so that you can be cautious in your credit decisions. Following are the 14 most common crediting traps that you need to beware of:

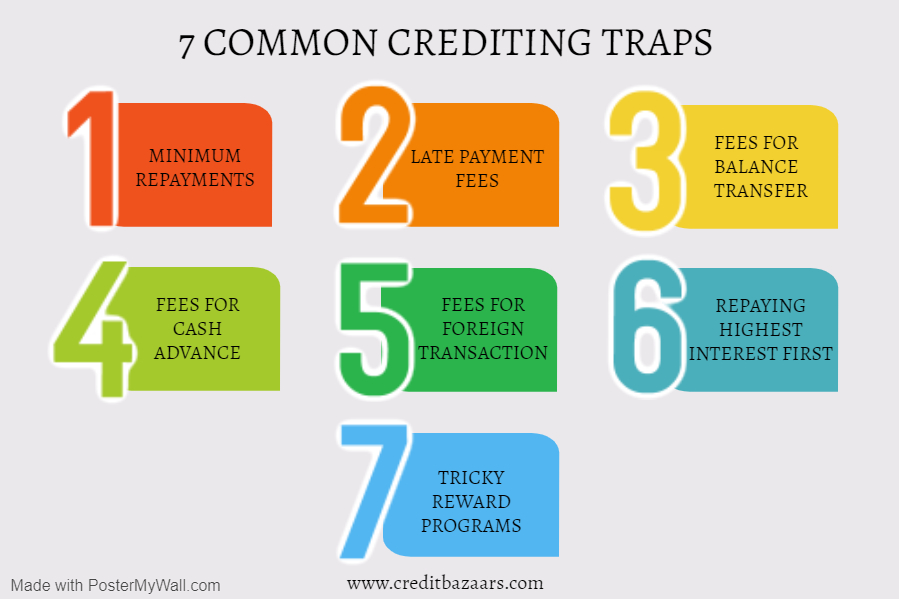

- MINIMUM REPAYMENTS: As all the credit card users know, that every month you have to make the minimum repayment that can vary from 1% to 3% of your whole balance. This helps you to evade the late payment fees, however, it will not help you to compensate your debt faster. This is because you still have to pay 97% of your balance, even though you have disbursed 3% of your balance. And this remaining 97% will accrue interest now. It might be difficult for you to pay your whole balance amount by the due date of your statement, though, you must try to pay as much as you can. This will aid you in avoiding unmanageable debt that you can accrue all at once and will also reduce the overall interest amount. The other option you can opt for is to transfer a balance with a 0% intro annual percentage rate of charge (APR) period credit card.

- LATE PAYMENT FEES: You will be charged a late payment fee when you fail to make the least minimum repayment. This cost will keep on adding every month and also leave negative markings on your credit. On the whole, this will lead to a decrease in your credit score and it can be difficult for you to apply for loans in the future. You can be charged quite an amount if you make your credit card payments late perpetually, as you will also be charged over-limit fees for the same for not paying your credit card bill on time.

- FEES FOR BALANCE TRANSFER: When being faced with a problem of paying off existing debt, you can utilize a balance transfer for moving your debt to a card with 0% interest for a promotional period. This will help to pay off your debt faster and save on interest costs as well. While you do not have to pay any interest for this promotional period, many of these cards come with a fee for a balance transfer. This fee is applied when your balance is moved for the first time and is generally either 3-5% of the full balance amount. So if your debt amount is Rs.5000 with a 3% balance transfer fee that would cost you Rs.150.

- FEES FOR CASH ADVANCE: Are you comfortably making cash advances using your card? Just whiling away withdrawing cash from ATMs or making gambling transactions? How much ever peaceful all these activities may sound, let us warn you, that they can be extremely expensive. This is because high-interest rates about 22-28% are levied on cash advances. Furthermore, contrasting to purchases, cash advances start to collect the interests also instantly. Also, many credit cards charge a 3-5% fee for utilizing your cash advances. This can be avoided if you use your debit card for ATM withdrawals or even a credit card that is issued by a credit union. The latter usually comes with a waived cash advance fee.

- FEES FOR FOREIGN TRANSACTION: So, you want to make overseas purchases? It is not a cakewalk as you might have to pay the foreign transaction fee, which can be anywhere between 1-3%. This is charged on the stuff you purchase overseas as well as when you do online shopping with an international retailer. There is hack here, that if you know you are going to travel internationally for work, leisure or are a regular shopper of international retailers online, you could consider getting a 0% foreign transaction fee credit card, which will cut back on this additional cost.

- REPAYING HIGHEST INTEREST FIRST: The bank must allocate your payment towards the debt amount. This means that the highest interest rate is collected first. This is done to assist you to avoid high-interest costs; however, it can also work against you. For instance, if you are paying off a particular debt with a 0% balance transfer offer, but at the same time, use the card for making a purchase. Then, your repayments will be used to paying off your purchases instead of disbursing your balance transfer. Just make sure where your payments are going, so that your 0% period is not wasted.

- TRICKY REWARD PROGRAMS: Generally, credit cards are linked with reward programs that entice the cardholders to spend more, for earning reward points that can be later redeemed for cash back or free flights. In this way, your plastic spending is rewarded in a great way if you are paying your balance in full every month. Though, the interest rates are too high for such cards. If you have a habit of carrying the balance from month to month, the interest you’ll have to pay can easily overshadow the rewards earned by you. In such a situation, it’s better that you consider a card with a less purchase interest rate.

CONCLUSION: Credit Bazaar provides you wide-ranged assistance, offering solutions to all your credit woes. We make sure that you do not fall into all the above common crediting traps that are common in today’s financial scenario. By making accurate and timely decisions, you can be vigilant and handle your credit wisely. We provide various Bazaar Improvement Plans for your credit assistance so that you can demonstrate positive credit behavior and increase your credit score.

For any queries regarding Credit Score improvement or Loan contact Credit Bazaar CR Arcade 2nd Floor, Opposite Delta Garden, Next to Shree Mahalaxmi Restaurant, Mira Road East, Thane: 401107